- FIDELITY VIEWPOINTS

- – 07/29/2019

See 3 ways that may help married couples boost their lifetime benefits.

93% who voted found this helpful

Key takeaways

| A couple with similar incomes and ages and long life expectancies may want to consider maximizing lifetime benefits by both delaying their claim.For couples with big differences in earnings, consider claiming the spousal benefit, which may be better than claiming your own.A couple with shorter life expectancies may want to consider claiming earlier. |

Married couples may have some advantages when deciding how and when to claim Social Security. Even though the basic rules apply to everyone, a couple has more options than a single person because each member of a couple1 can claim at different dates and may be eligible for spousal benefits.

Making the most of Social Security requires some strategy to take advantage of the basic benefit rules, however. After you reach age 62, for every year you postpone taking Social Security (up to age 70), you could receive up to 8% more in future monthly payments. (Once you reach age 70, increases stop, so there is no benefit to waiting past age 70.) Members of a couple may also have the option of claiming benefits based on their own work record, or 50% of their spouse’s benefit. For couples with big differences in earnings, claiming the spousal benefit may be better than claiming your own.

What’s more, Social Security payments are guaranteed for life and should generally adjust with inflation, thanks to cost-of-living increases. Because people are living longer these days, a higher stream of inflation-protected lifetime income can be very valuable.

But to take advantage of the higher monthly benefits, you may need to accept some short-term sacrifice. In other words, you’ll have less Social Security income in the first few years of retirement in order to get larger benefits later.

“As people live longer, the risk of outliving their savings in retirement is a big concern,” says Ann Dowd, a CFP® and vice president at Fidelity. “Maximizing Social Security is a key part of how couples can manage that risk.”

A key question for you and your spouse to discuss is how long you each expect to live. Deferring when you receive Social Security means a higher monthly benefit. But it takes time to make up for the lower payments foregone during the period between age 62 and when you ultimately chose to claim, as well as for future higher monthly benefits to compensate for the retirement savings you need to tap into to pay for daily living expenses during the delay period.

But when one spouse dies, the surviving spouse can claim the higher monthly benefit for the rest of their life. So, for a couple with at least one member who expects to live into their late 80s or 90s, deferring the higher earner’s benefit may make sense. If both members of a couple have serious health issues and therefore anticipate shorter life expectancies, claiming early may make more sense.

How likely are you to live to be 85, 90, or older? The answer may surprise you. Longevity has been steadily increasing, and surveys show that many people underestimate how long they will live. According to the Social Security Administration (SSA), a man turning 65 today will live to be 84.3 on average and a woman will live to be 86.6 on average. For a couple at age 65, the chances that one person will survive to age 85 are more than 75%. Further, the SSA estimates that 1 in 4 65-year-olds today will live past age 90, and 1 in 10 will live past age 95.2

Tip: To learn about trends in aging and people living longer, read Viewpoints on Fidelity.com: Longevity and retirement

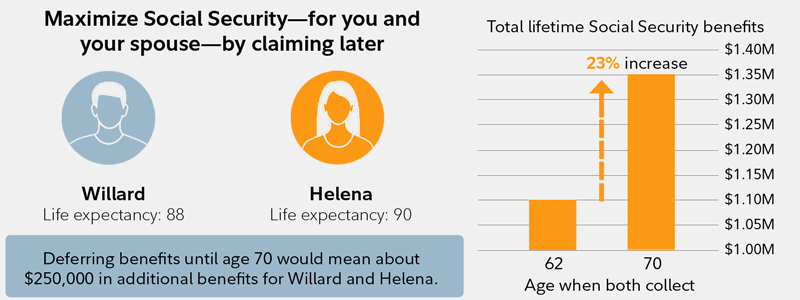

Strategy No. 1: Maximize lifetime benefits

A couple with similar incomes and ages and long life expectancies may maximize lifetime benefits if both delay.

How it works: The basic principle is that the longer you defer your benefits, the larger the monthly benefits grow. Each year you delay Social Security from age 62 to 70 could increase your benefit by up to 8%.

Who it may benefit: This strategy works best for couples with normal to high life expectancies with similar earnings, who are planning to work until age 70 or have sufficient savings to provide any needed income during the deferral period.

Example: Willard’s life expectancy is 88, and his income is $75,000. Helena’s life expectancy is 90, and her income is $70,000. They enjoy working.

Suppose Willard and Helena both claim at age 62. As a couple, they would receive a lifetime benefit of $1,100,000. But if they live to be ages 88 and 90, respectively, deferring to age 70 would mean about $250,000 in additional benefits.

All lifetime benefits are expressed in today’s dollars, calculated using life expectancies of 88 and 90 for husband and wife, respectively. The numbers are sensitive to life expectancy assumptions and could change.

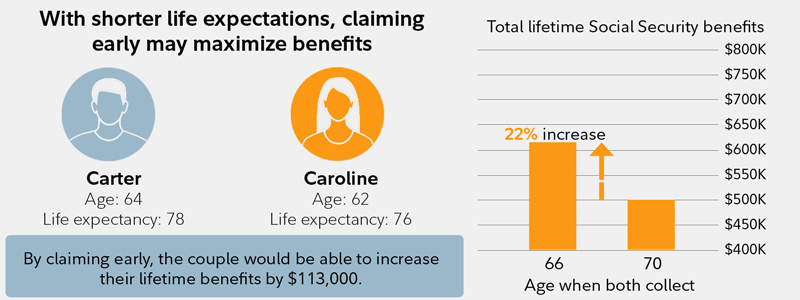

Strategy No. 2: Claim early due to health concerns

A couple with shorter life expectancies may want to claim earlier.

How it works: Benefits are available at age 62, and full retirement age (FRA) is based on your birth year.

Who it may benefit: Couples planning on a shorter retirement period may want to consider claiming earlier. Generally, one member of a couple would need to live into their late 80s for the increased benefits from deferral to offset the benefits sacrificed from age 62 to 70. While a couple at age 65 can expect one spouse to live to be 85, on average, couples who cannot afford to wait or who have reasons to plan for a shorter retirement, may want to claim early.

Example: Carter is age 64 and expects to live to 78. He earns $70,000 per year. Caroline is 62 and expects to live until age 76. She earns $80,000 a year.

By claiming at their current age, Carter and Caroline are able to maximize their lifetime benefits. Compared with deferring until age 70, taking benefits at their current age, respectively, would yield an additional $113,000 in benefits—an increase of nearly 22%.

All lifetime benefits are expressed in today’s dollars, calculated using life expectancies of 78 and 76 for husband and wife, respectively. The numbers are sensitive to life expectancy assumptions and could change.

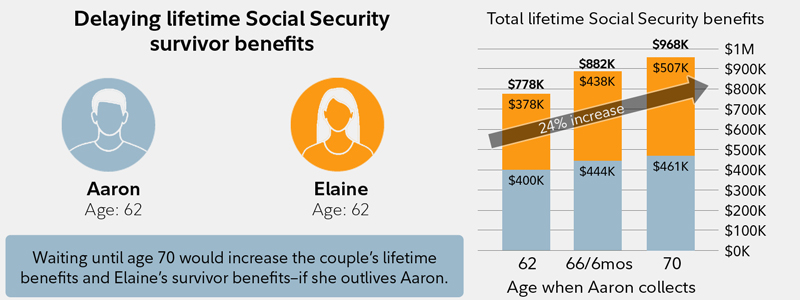

Strategy No. 3: Maximize the survivor benefit

Maximize Social Security—for you and your spouse—by claiming later.

How it works: When you die, your spouse is eligible to receive your monthly Social Security payment as a survivor benefit, if it’s higher than their own monthly amount. But if you start taking Social Security before your full retirement age (FRA), you are permanently limiting your partner’s survivor benefits. Many people overlook this when they decide to start collecting Social Security at age 62. If you delay your claim until your full retirement age—which ranges from 66 to 67, depending on when you were born—or even longer, until you are age 70, your monthly benefit will grow and, in turn, so will your surviving spouse’s benefit after your death. (Get your full retirement ageOpens in a new window)

Who it may benefit: This strategy is most useful if your monthly Social Security benefit is higher than your spouse’s, and if your spouse is in good health and expects to outlive you.

Example: Consider a hypothetical couple who are both about to turn age 62. Aaron is eligible to receive $2,000 a month from Social Security when he reaches his FRA of 66 years and 6 months. He believes he has average longevity for a man his age, which means he could live to age 85. His wife, Elaine, will get $1,000 at her FRA of 66 years and 6 months and, based on her health and family history, anticipates living to an above-average age of 94. The couple was planning to retire at 62, when he would get $1,450 a month, and she would get $725 from Social Security. Because they’re claiming early, their monthly benefits are 27.5% lower than they would be at their FRA. Aaron also realizes taking payments at age 62 would reduce his wife’s benefits during the 9 years they expect her to outlive him.

All lifetime benefits are expressed in today’s dollars, calculated using life expectancies of 85 and 94 for husband and wife, respectively. The numbers are sensitive to life expectancy assumptions and could change.

If Aaron waits until he’s 66 years and 6 months to collect benefits, he’ll get $2,000 a month. If he delays his claim until age 70, his benefit—and his wife’s survivor benefit—will increase another 28%, to $2,560 a month. (Note: Social Security payout figures are in today’s dollars and before tax; the actual benefit would be adjusted for inflation and possibly subject to income tax.)

Waiting until age 70 will not only boost his own future cumulative benefits, it will also have a significant effect on his wife’s benefits. In this hypothetical example, her lifetime Social Security benefits would rise by about $69,000, or 16%.

Even if it turns out that Elaine is overly optimistic and she dies at age 90, her lifetime benefits will still increase approximately 34% and she would collect approximately $129,000 more in Social Security benefits than if they had both claimed at 62 (vs. both waiting until age 70 to claim Social Security).

In situations where the spouse’s Social Security monthly benefit is greater than their partner’s, the longer a spouse waits to claim Social Security, the higher the monthly benefit for both the spouse and the surviving spouse. For more on why it’s often better to wait until at least your FRA before claiming Social Security, read Viewpoints on Fidelity.com: Should you take Social Security at 62?

In conclusion

Social Security can form the bedrock of your retirement income plan. That’s because your benefits are inflation-protected and will last for the rest of your life. When making your choice, be sure to consider how long you may live, your financial capacity to defer benefits, and the impact it may have on your survivors. Consider working with your Fidelity financial advisor to explore options on how and when to claim your benefits.

Next steps to consider

Call or visit to set up an appointment.

Estimate Social Security

Answer 5 simple questions to estimate when to claim your benefits.

Get help with your plan

Create a retirement income plan in our Planning & Guidance Center.Was this helpful? YesNo93% who voted found this helpful

Sign up for Fidelity Viewpoints®

Get a weekly email of our pros’ current thinking about financial markets, investing strategies, and personal finance.First NameLast NameEmailSubscribe

This information is intended to be educational and is not tailored to the investment needs of any specific investor.This article uses the Annuity 2000 mortality table to determine longevity, which is a narrower universe than the Social Security Administration’s. The Social Security Administration uses a mortality table that averages the entire nation. The Annuity 2000 table better reflects the typical Fidelity client, skewing toward a somewhat more educated and affluent individual with a slightly longer life span.1. On June 26, 2015, the U.S. Supreme Court issued a decision in Obergefell v. Hodges, holding that same-sex couples have a constitutional right to marry in all states and have their marriage recognized by other states. This ruling made it possible for same-sex couples to benefit from SSA programsOpens in a new window.2. https://www.ssa.gov/planners/lifeexpectancy.htmlOpens in a new windowLifetime benefits are determined by calculating the present values of the Social Security payments over time. The present values are calculated by discounting the Social Security payouts by an inflation-adjusted rate of return. The illustrations use the historical average yield of U.S. 10-Year TIPS for discounting.The benefit calculations and discounting in this article do not account for the effect of taxes. The after-tax discount rate for an individual could be very different from another depending on multiple factors, including the sources and levels of income. For individualized estimates, one could try the Retirement Estimator from the Social Security Administration. It assumes a person is in good health. Average longevity corresponds with a 50% chance of living to a stated age. Above-average longevity corresponds with a 25% chance of living to a stated age.The information contained herein is general in nature, is provided for informational purposes only, and should not be construed as legal or tax advice. Fidelity does not provide legal or tax advice. Fidelity cannot guarantee that such information is accurate, complete, or timely. Laws of a particular state or laws that may be applicable to a particular situation may have an impact on the applicability, accuracy, or completeness of such information. Federal and state laws and regulations are complex and are subject to change. Changes in such laws and regulations may have a material effect on pretax and/or after-tax investment results. Fidelity makes no warranties with regard to such information or results obtained by its use. Fidelity disclaims any liability arising out of your use of, or any tax position taken in reliance on, such information. Always consult an attorney or tax professional regarding your specific legal or tax situation.

Past performance is no guarantee of future results.Investing involves risk, including risk of loss.Votes are submitted voluntarily by individuals and reflect their own opinion of the article’s helpfulness. A percentage value for helpfulness will display once a sufficient number of votes have been submitted.

Fidelity Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917702419.7.2

Leave a comment