The Section 199 deduction (also referred to as the domestic manufacturing deduction, U.S. production activities deduction, and domestic production deduction) is a tax break for businesses that perform domestic manufacturing and certain other production activities. It was established by the American Jobs Creation Act of 2004 in an effort to ease the tax burden of domestic manufacturers and as a result, make the investment in domestic manufacturing facilities more advantageous.

What activities are eligible for the Section 199 deduction?

Per Section 199, domestic production gross receipts (DPGR) can be derived from the following qualifying production activities as long as they are conducted in whole or in significant part within the U.S.:

- The manufacture, production, growth, or extraction by the taxpayer of tangible personal property. This encompasses all tangible personal property (except land and building), computer software, and sound recordings.

- The production of qualified film

- The production of electricity, natural gas, or water

- The construction of real property

- The services of architecture/engineering

DPGR resulting from the property produced must be owned by the producer taking the deduction (i.e. the production of property that is owned and under contract by someone else would generally not be eligible).

How is the Section 199 deduction calculated?

The deduction is limited to the income produced by the above qualifying activities. Income from qualified production activities is calculated as domestic production gross receipts (DPGR) less cost of goods sold and other expenses that are directly allocable to the production of DPGR. Income and expenses that are not directly related to qualifying activities will need to be backed out of the calculation of qualified production activity income. After the lesser of the DPGR or taxable income is multiplied by the applicable percentage (9% for 2010), the deduction is further limited to 50% of Form W-2 wages allocable to DPGR.

The Section 199 deduction is allowed for both regular and alternative minimum tax for individuals, C corporations, farming cooperatives, estates, trusts, and their beneficiaries. The deduction is also allowed at the partner, member, and owner level for a partnership, LLC, and S corporations, respectively. Businesses should also be aware that the Section 199 deduction does not always apply at the state level. As of the beginning of 2010, 22 states (including Indiana) have departed from the federal deduction.

The following are some examples of how the Section 199 deduction would be calculated in certain circumstances:

Example #1: For the year ended December 31, 2010, Kim”s Manufacturing Company (a C-Corp) had taxable income, all from qualifying manufacturing activities, of $1 million and paid $100,000 in W-2 wages.

Example #1 Solution: Kim will be entitled to a Section 199 deduction of $50,000 due to the 50% limit of W-2 wages. If the W-2 wages had been greater than $180,000, the deduction would have been $90,000 [$1 million X 9%].

Example #2: Same facts as #1 ($180k W-2 wages), except Kim’s Manufacturing Company is a S-Corp, with Kim owning 60% and Choi owning 40%.

Example #2 Solution: The deduction passes through to the shareholders, with Kim receiving $54,000 and Choi receiving $36,000 of the deduction.

Example #3: Same facts as #2, except that Kim takes a $108,000 distribution and Choi takes a $72,000 distribution. No W-2 wages are paid.

Example #3 Solution: A Section 199 deduction can’t be taken because W-2 wages were not paid.

What are some specific applications of the Section 199 deduction to the Manufacturing Industry?

Qualified production property (QPP) includes all tangible personal property, except land and buildings, and includes computer software and sound recordings. Qualified manufacturing activities will include those which, manufacture, produce, develop, improve, install, grow, extract and/or create the qualifying production property. Even those processes that use scrap, salvages, or junk material (instead of new or raw material), may be eligible. Such produced material will be eligible if it is processed, manipulated, refined, or altered such that the materials form is changed or the material is combined/assembled into two or more articles or materials. Furthermore, manufacturing components that will later be used by another party for manufacturing or product activities will be considered eligible.

Below are some of the other examples

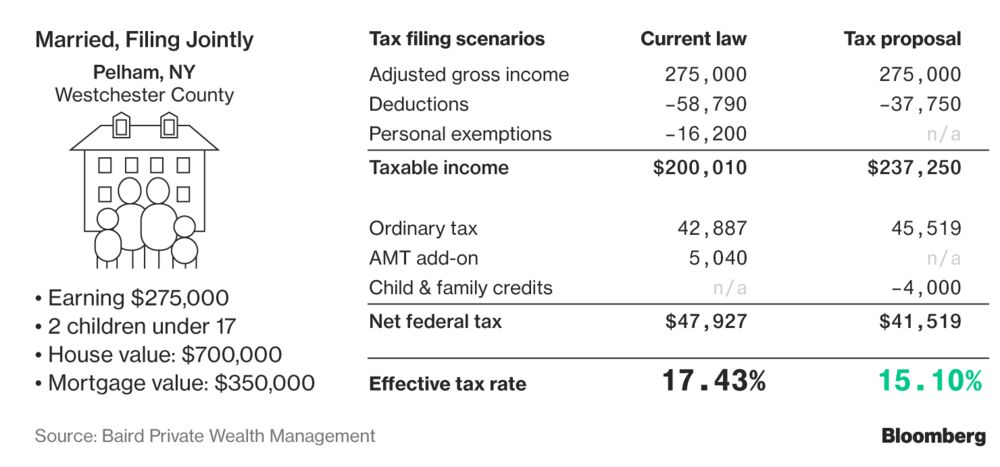

The Suburban Family in Westchester

A married couple in a New York suburb has estimated state income tax of $17,290; their annual mortgage interest deduction is $14,000; and they pay property tax of $13,750—about the same amount they donate to charity.

While the bill takes a bite out of this family’s deductions and exemptions, they would benefit from enhanced child tax credits and avoiding the alternative minimum tax, or AMT. (The bill would raise the thresholds at which the AMT applies—until 2026.)

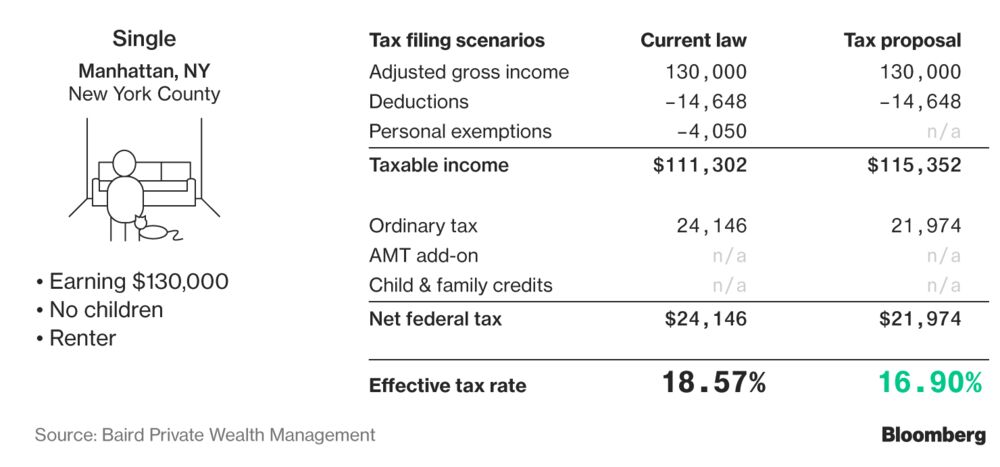

Single in Manhattan

This New York renter pays estimated state income tax of $8,148 and gives about $6,500 to charity.

The final tax legislation is more generous to this taxpayer than the bills that originally passed the House and Senate. That’s because it permits the deduction of state and local income taxes up to $10,000. The original proposals scrapped the income tax deduction entirely and allowed only a $10,000 deduction for property taxes, which this renter doesn’t pay.

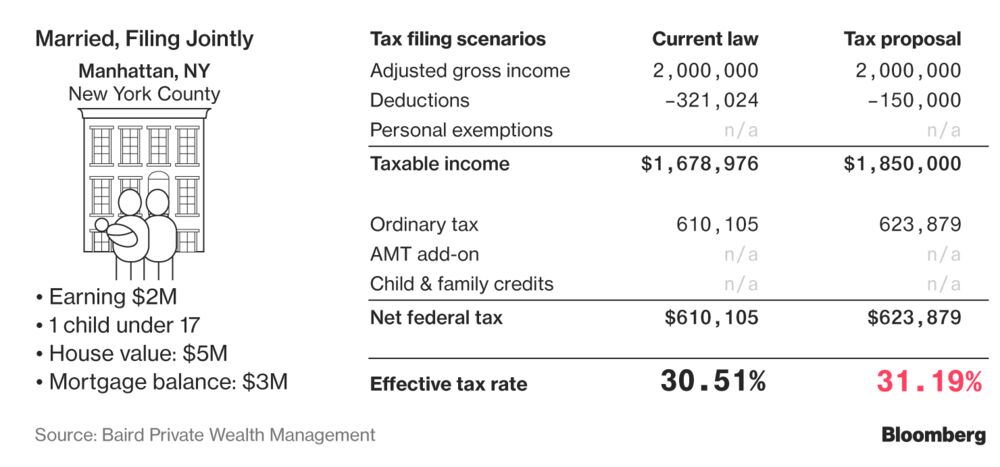

The Multimillionaires in New York

These Manhattan residents have a jumbo mortgage (at an assumed 4 percent interest rate) and take a $40,000 deduction on mortgage interest; pay property taxes of $96,250 and state income tax of $135,360; and make annual charitable contributions totaling $100,000.

They will pay a bit more next year because they would lose key deductions, especially the ability to put down more than $10,000 in state and local taxes. That offsets a drop in the top marginal tax rate, from 39.6 percent to 37 percent. (The “marginal rate,” the rate paid on any extra dollar earned, is different from the “effective tax rate,” which is the overall, blended rate you pay as different tax rates are levied on your income at different thresholds.)

City taxes for these Manhattan dwellers would work out to almost 4 percent. Combine that with the top federal rate and top state rate, and you get a marginal rate approaching 50 percent.

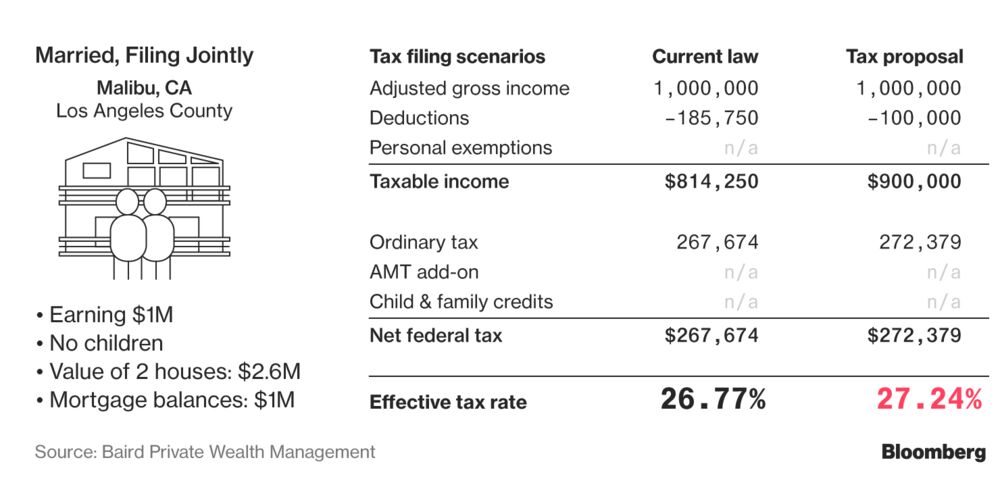

The Second-Home Scenario in California

A married couple has a primary residence in Malibu, California, and a second home in Lake Tahoe. The property tax on the Malibu home is $15,860, and they pay $4,896 on their second home; they deduct a total of $40,000 in mortgage interest for the two homes; and they give $50,000 to charity.

This couple would lose almost $86,000 in deductions under the tax bill. Nonetheless, other changes—especially the drop in the top tax rate—means their effective tax rate creeps up by only 0.5 percentage points.